US CPI Drop Shakes Markets

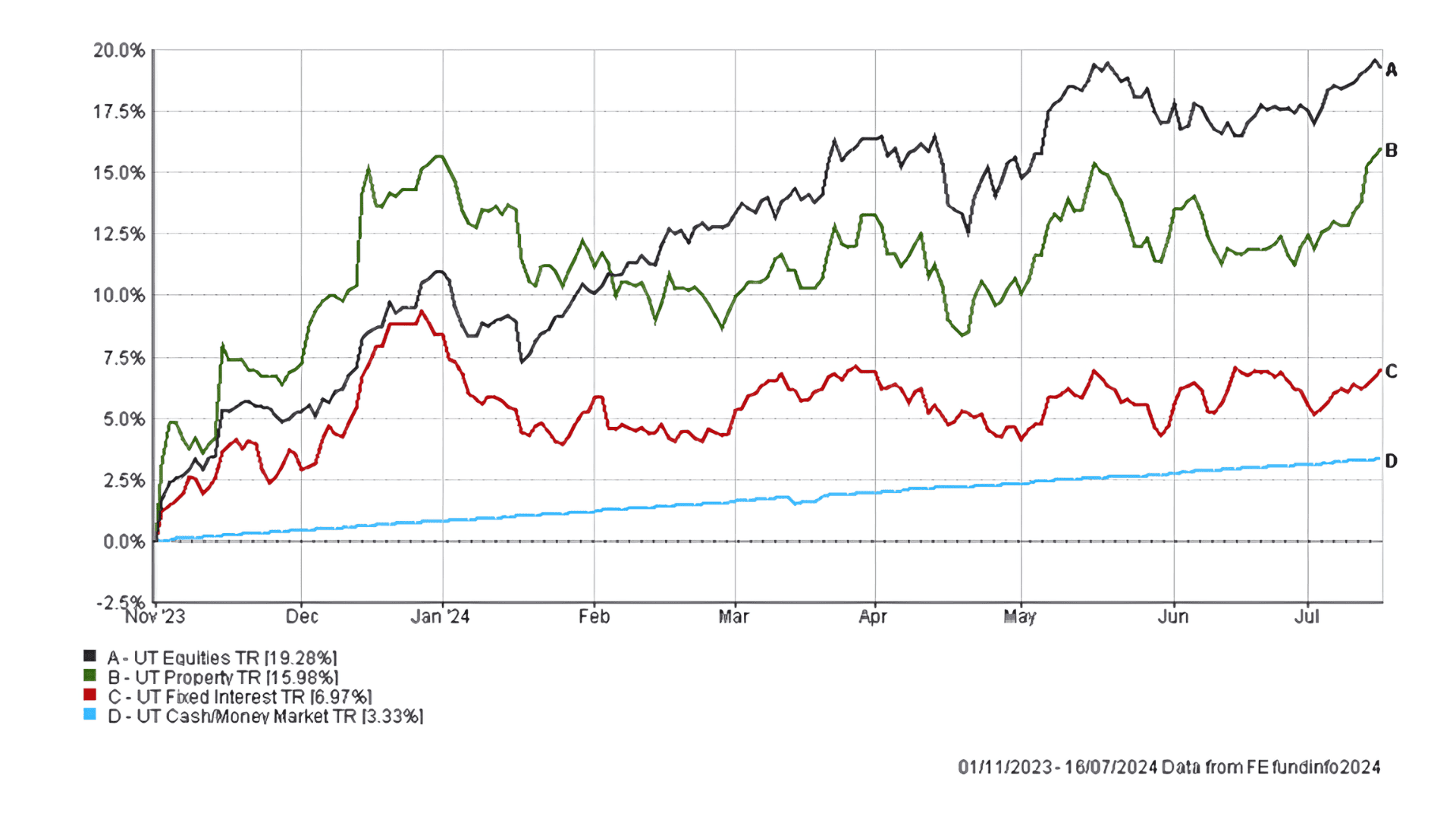

This update covers the period up to 17 July 2024, though with the last update, we have taken the basic asset class chart (fig.1) back to the end of October last year, the latest Powell pivot.

Asset Class Performance Since the Last Powell Pivot > 01/11/2023 – 17/07/2024 (fig.1)*

Macro

With Canada cutting interest rates last month, quickly followed by the ECB, it’s little surprise the eyes of the world are locked on the world’s biggest central banks to see if they will soon follow suit. However, unlike in the UK, where CPI inflation recently fell beneath the Bank of England’s 2% target, in the US – up until last week – it has proved stickier, loitering over 3%.

At this level, the consensus was that the Federal Reserve may adopt a cautious approach to interest rate cuts. That was until Thursday, 11 July, when it was announced that the US Consumer Price Index (CPI) came in below expectations in June, rising 3% annually. This sparked huge debates about whether the Fed needed to act quicker in cutting rates and sent huge ripples through the US stock market.

In the immediate aftermath, we saw one of the most significant recorded swings from the Nasdaq to the Russell 2000, as markets continued their recent track record of not behaving in the way we should expect in both rising and falling interest rate environments.

With the US, and by proxy global markets, being so dominated in the recent past by the Magnificent Seven, the most significant thing to take away from last week’s market moves was that it signifies a general change in the direction of travel for equities. There has been a sense of change in what moves markets, and, as ever, all roads lead to diversification.

As medium to long-term investors, our job is to look at the wider trends, as opposed to when the first interest rate cut will be, because it is meaningless in the larger scheme of things. Instead, we look to take advantage of underpriced assets in absolute and relative terms, which is what we have been doing in US small caps since last year.

Portfolio Performance & Positioning

While, in general, we have been bearish on some US equities for a period of time, in August last year, we started buying into smaller US companies because they looked relatively attractive in terms of valuation compared with their larger-cap peers. We were not trying to time markets because we didn’t know when there would be change, and despite last week’s market moves, we still don’t, as it could be just a blip.

In the last few days, we have seen new headwinds for the US giant tech stocks that have emerged. Firstly, the Biden administration is considering bringing wide raging restrictions on chip stocks in an effort to stymy China, but actions that would undoubtedly hinder the US companies involved. We have warned for years now that companies operating at record stock price levels are subject to negative newsflow, which could be anything from sanctions to anti-trust legislation to an administration that doesn’t really like you, for example, Trump’s dislike for Facebook CEO Mark Zuckerburg. The stocks in the Magnificent Seven all have their idiosyncrasies, but it would be difficult to argue that they are cheap at these levels, and some might say they are incredibly expensive.

Back to smaller companies and outside of the US, we have also been adding to European small cap weightings and maintaining our exposure to UK small caps, which has aided performance. At the same time, many of our all-cap fund managers have decent weightings to small caps, an area that has traditionally generated alpha.

We have been reducing our cash weighting and increasing our bond exposure outside of equities. Generally, the performance of active bond managers has been strong, and with signs that the UK economy is improving and a stronger pound, we have been adding to our gilt holdings.

Finally, having come slightly off its highs earlier in July, the price of gold rose again following the US CPI announcement. Gold has been our best-performing asset over the last three years, and it continues to benefit the portfolios because of its diversification benefits. In the first fifteen days of July, the gold miners we own were up close to 15%, which has benefitted performance overall. We still maintain that there is much more value to come in gold. This asset class traditionally performs poorly in a higher interest rate environment because it doesn’t yield anything. Despite this, the price of gold keeps setting record after record, and this is because of the different dynamics at work with the central bank buying and wider afield; we still think there are many opportunities in commodities and everything associated with them.

Investor Outlook

A look at regional and sector performance over the last month reveals that on a weekly basis, different areas are coming to the fore. One week, the US small caps were the best performing area; the previous week, it was the Hang Seng index in Hong Kong, and before that, Japan was at the top of the charts.

This demonstrates that as investors, we need to be diversified and look at the relatively undervalued areas. Valuations outside the most expensive regions remain reasonable, suggesting potential for positive returns in bonds, property, and infrastructure.

While fixed income assets may continue to be volatile from here, attractive yields, low valuations and the potential for capital growth are a potent mix for such an unloved asset class, and we all know the perils of trying to invest based on conditions that are now in the rearview mirror.

Overall, avoiding complacency and maintaining a diversified investment approach across all asset classes is essential.

*Information is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 146.7.24