Will Markets Keep Their Cool During Election Heat?

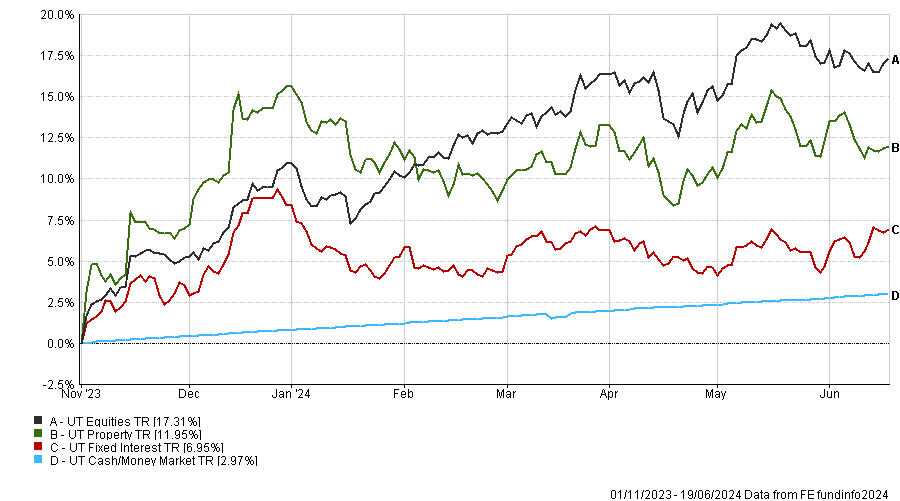

This update covers the period up to 19 June 2024, though as with the last update, we have taken the basic asset class chart (fig.1) back to the end of October last year, the latest Powell pivot.

Interestingly, so far in June, we have seen a pick-up in sovereign bonds, which is an outcome, despite the central banks regaling us with almost daily updates, which all appear designed to move the markets as they want. Most of the latest attempts at moving prices have been to continue rowing back on the narrative started by Fed Chair Powell back in October 2023. That was the last specific pivot point, which you can clearly see in asset class returns.

The commentary since then has been more akin to slow torture and cloaked in ‘data dependence’. It’s hard to comprehend, other than in a crisis, why there would ever be a strategy that was not data-dependent. The alternative is what – “we are data agnostic”?

Asset Class Performance Since the Last Powell Pivot > 01/11/2023 – 19/06/2024 (fig.1)*

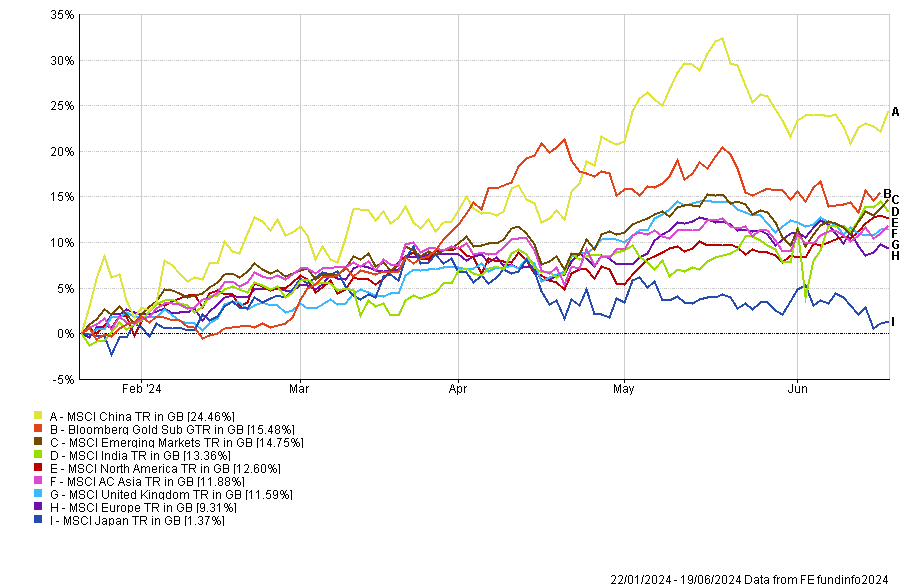

China’s latest market positive impulse, which commenced on January 22, 2024, stalled in the middle of May (fig.2). However, unlike the last two attempts to join in the global equity rally, this time the markets held up relatively well in absolute terms.

The data out of China, while not earth-shattering, is relatively positive. While Europe and the US compete to slap ever greater tariffs on Chinese companies, in Q1 of this year, there was a record amount of intra-Asia trade.

It has been a similar story for gold, which halted its record-breaking run but has barely given back any of its advance. We remain optimistic about gold and the whole commodity complex for many reasons.

For anybody who would like more information or to discuss why we feel that much of the commodity complex is now in an enforced supercycle, please reach out to us at enquiries@ibossltd.co.uk.

MSCI Country & Gold Performance since China’s Resurgence > 22/01/2024 – 19/06/2024 (fig.2)*

Macro

UK election fever is now in full swing. The TV debates have started, and all the major parties have put pen to paper on their manifestos, with proposed changes to taxation and VAT on private school fees all making headlines in the press.

Of course, much has already been written this year about how much of the world’s population is going to or, in the case of India, has been to the polls. This always leads to questions about what impact these events might have on markets, and our answer remains the same: it is minimal.

Let’s take India as an example. At the start of the month, the National Democratic Alliance (NDA) coalition won the 2024 Indian election, with Prime Minister Narendra Modi set to secure a third term in power. The result was much tighter than exit polls suggested, and in the immediate aftermath, the Sensex index of Indian stocks fell over 8%.

However, while politics in India is interesting, perhaps more noteworthy is that, as a region, it is more highly valued than even the US. Things can quickly go wrong when you have an expensive market and volatility increases. However, after the initial sharp reaction, markets rebounded, and in the end, as with most elections, the overall impact was quite limited. We often get asked about India in the context of India or China from here? We believe you should have an allocation to both of these globally significant economies, and we do so via both our active and passive fund allocations to global emerging markets and Asia.

Let’s take this to the UK, which will have already gone to the polls by our next monthly update. The anecdotal evidence we get is that while domestic investors are selling UK equities, international investors are buying for the first time in a long time. This could demonstrate that being based in the UK means we all get caught up in all that noise, but from the international viewpoint, the UK election is one of the least controversial political events this year.

After Brexit and six years of being the most controversial area from a political point of view, a period of being seen as boring has to be a positive for the UK. Indeed, the UK has been outperforming since markets bottomed in 2022, and from the start of 2024, UK smaller companies have been one of the best-performing sectors.

So, while the ideal scenario for the UK is that not much happens and everything goes as expected, ultimately, whatever the election outcome, we feel it will be the relatively cheap valuations that have a real long-term impact on investor returns.

Portfolio Performance & Positioning

Looking at performance, one thing to note is the vast dispersion in the best and worst-performing active funds in each of the major regions. If we take the UK, the best fund year-to-date is up 22.21%, while the worst is down 1.59%. Meanwhile, the top-performing active fund in the US is up 22.13%, while the bottom-ranked fund is down 8.35%.

What is interesting here is the similarity in performance between each in the major regions, with the best-performing funds in the UK, US, Japan and Europe each up close to 22%, which is a strange coincidence. At the same time, while the US has been the best-performing region this year, our underweight to the region has had limited impact on IBOSS performance this year, where all core portfolios remain ahead of their respective benchmarks.

For the first time in a long time, performance has not been driven entirely by asset allocation but instead by fund selection. In the UK, we try to pick managers with a broad investment remit. Good examples are the Artemis UK Select and the Polar Capital UK Value Opportunities fund, which have performed strongly recently as a more comprehensive selection of UK stocks have performed better. We continue to favour active managers in the UK and expect they should be well placed to take advantage of increased direct foreign investment should the UK persist on its path to relative stability.

Finally, we have been increasing our allocation to fixed income assets. While they may continue to be volatile from here, attractive yields, low valuations and the potential for capital growth are a potent mix for such an unloved asset class.

Investor Outlook

We believe that investors will continue to be rewarded for holding a diversified selection of risk assets. It is worth remembering that diversification is not only about reducing risk but can also contribute to attractive total returns. Alongside our longer-term data, the last 18 months have proven that concept, and most IBOSS portfolios have outperformed since the market lows of November 2022.

After ten years of barely outperforming cash, we think bonds now present an incredible opportunity, offering the potential for sizeable yield and capital returns. In addition, the downside for these assets looks to be more limited than before, and if equities were to struggle, bonds could be the ideal asset to boost portfolio returns, at least on a relative basis.

This means that multi-asset portfolios, for the first time since 2020, look set to be rewarded for being truly multi-asset and do not need to be beholden to the performance of just equities or just bonds. This outlook will not be unduly affected by the outcome of the UK election on 4 July, and we believe that while markets may be volatile, equities and bonds represent significant opportunities from here.

*Information is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 132.6.24