What do Gold, China, and the UK All Have in Common?

This update covers the period up to 12th May 2024, though, as with the last update, we have taken the basic asset class chart (fig.1) back to the end of October last year; the latest Powell pivot.

With hindsight, it is clear that during the period, in broad terms, markets rallied as a first response to Fed Chair Jerome Powell’s celebratory reaction to the October news that inflation had fallen. There was then a period of consolidation, at least for property and bonds, as the confidence drained from Powell and other Fed members that the non-transitory inflation had been conquered.

Finally, all assets climbed further despite the Fed being all over the map when it came to signalling their inflation and interest rate expectations. The consensus was (and still is) that the peak for rates is in. While hundreds of hours, column inches, and a seemingly never-ending number of ‘fireside chats’ pontificate the meaning of Fed speak, much of the rest of the economic world continues to perform reasonably well.

Fig 1: Asset Class Performance Since the Last Powell Pivot > 01/11/2023 – 10/05/2024*

Macro

While many market commentators and the financial media appear blindsided by the Fed’s confusion, global markets have gone their own way. China has been chipping away at regulations and restrictions and trying to boost investor sentiment for quite a while now, and it finally appears to be showing some decent results (fig 2). Simultaneously, the much-maligned UK market has continued to be the developed world’s best performer. A third asset to add to the mix is gold, which, more than any other asset or geography, appears to have caught out many asset allocators and retail investors alike. In our industry, we are always looking for answers as clues, with hindsight to help tell us what happens next.

Fig 2: MSCI Country & Gold Performance since China’s latest Resurgence > 22/01/2024 – 10/05/2024*

So, what do gold, China, and the UK all have in common?

At first glance, the answer is arguably nothing, but there are some discernible factors. Firstly, the UK and China are unloved and, in some cases, even despised. In fact, if there are two tradable countries with a chronic PR problem, it’s these two. Secondly, and no doubt partly due to their unloved status, both equity markets are relatively cheap compared to countries that investors favour, such as the US or India.

The reason we look at gold similarly is that it has also seen (ETF) outflows and many investors seem to have given up on it. Like China and the UK, it is often misunderstood and suffers from endless re-categorisation from sometimes commodity to currency, to store of value, to the somewhat left-field ‘pet rock’. We like gold for its diversification benefits and access it via the NinetyOne Gold (miners) fund; we also like it as a small amount of insurance against further currency-destructive acts by governments and central banks. These institutions seem unconcerned about the rising debt piles or the immediate plight of their currencies. Generally speaking, we view gold as a long-term holding in the portfolios.

Amid the ongoing talk around American exceptionalism and the UK floundering around waiting for a new government, we thought it worth highlighting their relative performances. The date used on the chart is 1st November 2021, which was approximately when Powell’s Fed realised they had got the inflation story horribly wrong and launched the fastest rate rising cycle in modern history (fig 3). In fact, the UK as measured by the MSCI, has outperformed North America since October 2020.

Fig 3: MSCI United Kingdom vs. North America > 01/11/2021 – 10/05/2024*

As we enter the summer, the macro backdrop is decidedly mixed. Firstly, there are the ongoing physical wars in the Middle East and Ukraine, then there are wars of words, tariffs, and counter-tariffs, notably between the US and China, but also between many other countries. Sadly, none of these situations look like they will be resolved soon. It’s an uncomfortable truth that escalations are at least as likely as de-escalations between Russia and Ukraine and Israel and Hamas. Likewise, tariff talk will stay front and centre for years, if not perpetually, regardless of election outcomes.

Aside from these depressing observations, there is somewhat better news around many economies. Without going into detail, there is more promising data from Europe, the UK, China, India, Japan, and the US. This is undoubtedly good news on most fronts, but we cannot have everything at once. The stronger economic data portends higher inflation, therefore reducing the potential speed and magnitude of interest rate cuts. This overall positive, rather messy setting for investors could favour some of the best active managers until markets become more one-directional again.

These things cannot be timed, and the only option is to remain vigilant for any changes to market dynamics.

Portfolio Performance & Positioning

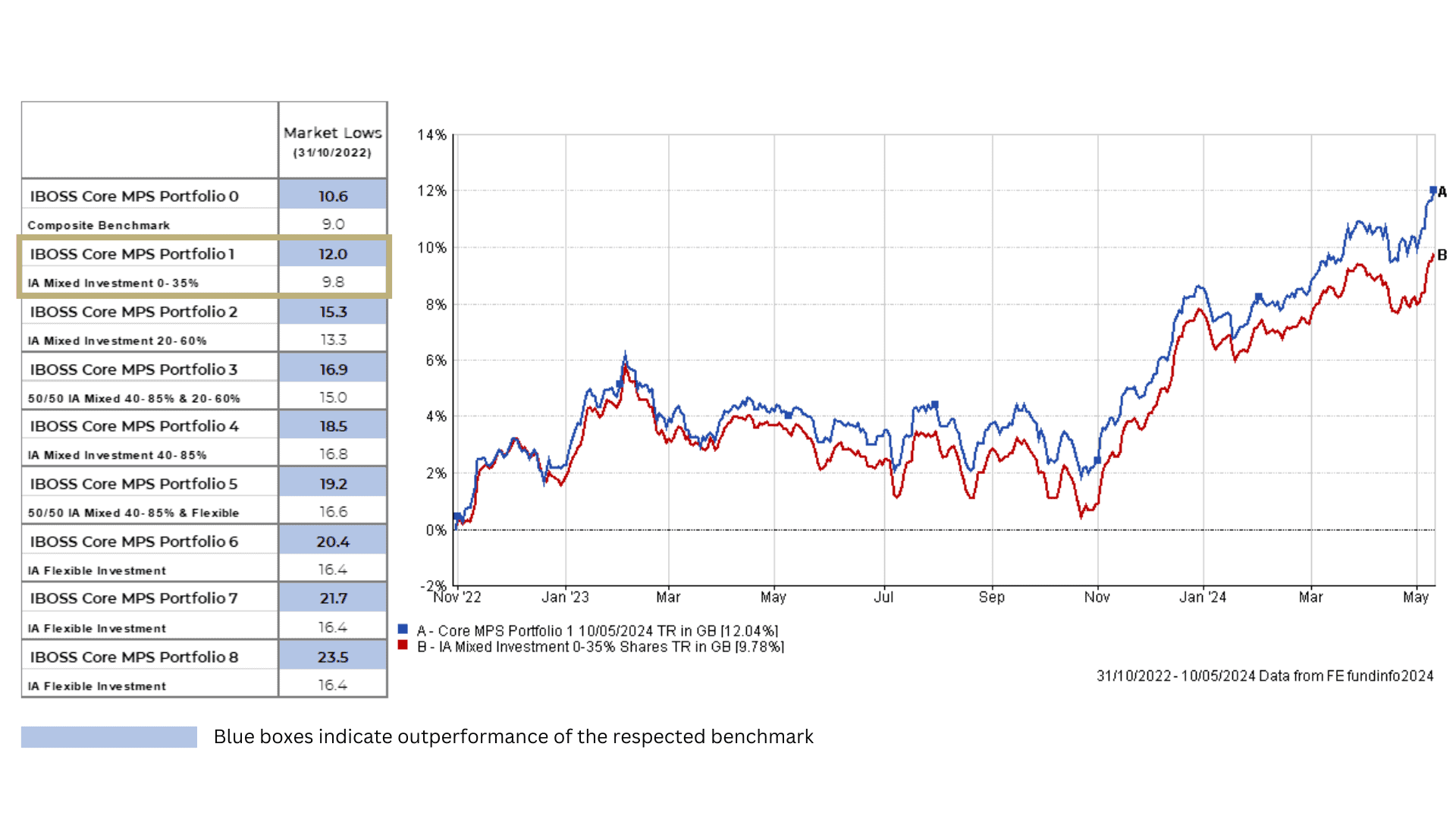

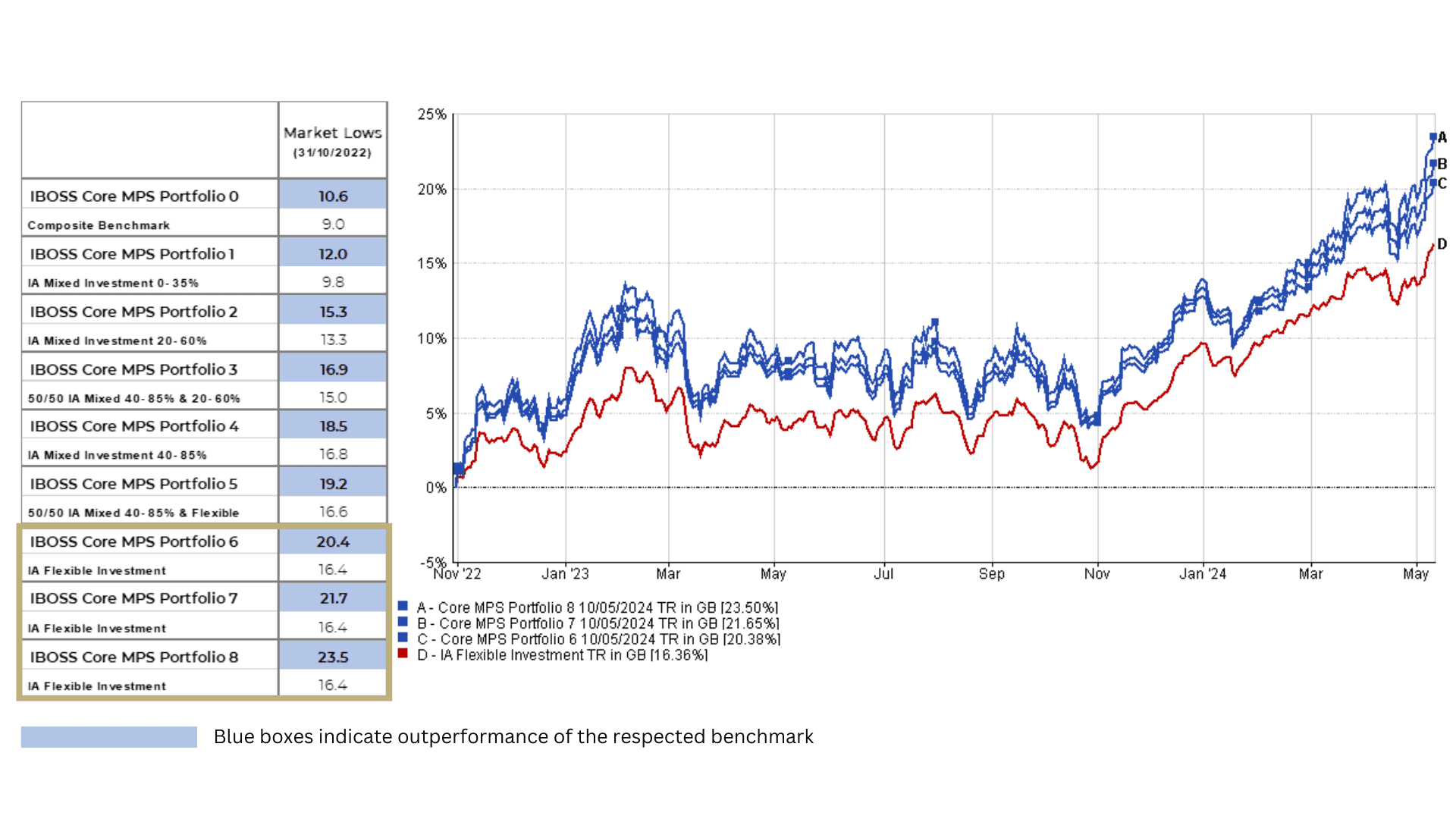

All of the Core portfolios have continued to outperform their relevant benchmark since market lows at the end of October 2022, as shown in figs 4, 5, 6, and 7 below.

As we are probably better known for our ability to protect clients in the market falls, such as the drop in lower-risk portfolios earlier in 2022, we again wanted to highlight our performance across the risk spectrum since the market lows of 2022.

As highlighted earlier, the market is now rewarding rather than penalising diversification in equities. We also see less definitive style bias leading markets with both value and growth having a more nuanced relationship, and this, again, should favour active managers who invest on a more blended basis.

In conclusion, with 15 years of performance to reflect on, we are confident that we are entering market conditions that significantly favour IBOSS’s investment approach.

Outperformance in a Rising Market

Fig 4: IBOSS Core MPS Portfolio 1 > 31/10/2022 – 10/05/2024*

Fig 5: IBOSS Core MPS Portfolio 2 > 31/10/2022 – 10/05/2024*

Fig 6: IBOSS Core MPS Portfolio 4 > 31/10/2022 – 10/05/2024*

Fig 7: IBOSS Core MPS Portfolio 6/7/8 > 31/10/2022 – 10/05/2024*

Investor Outlook

While some equity markets remain attractive, many areas of the fixed income complex have the most attractive risk-return profiles relative to their respective histories. As always, we know many clients will want to focus on the areas of investment that have done the best in the recent past. This rearview mirror approach to investing often produces disappointing results. Our approach aims to be much more forward-looking as our portfolios are positioned to take advantage of areas of future opportunity.

It may take some clients months, if not years, to realise that there is more to investing than US growth stocks (tech) but whilst they focus on the short term it is our job is to see the bigger picture and position accordingly. A large US financial institution that didn’t wish to be publicly named recently told us that they thought the era of US equity outperformance was ending and that ‘American exceptionalism’ would be extremely difficult to maintain in an environment of higher inflation, interest rates and deglobalisation. We are still bullish on much of the US markets, but we would agree that the bar for exceptionalism is now very high.

*Information is short term in nature to demonstrate performance over a specific time period. Please contact IBOSS for long term data, including since launch and/or 5 years.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Investments are intended to be held over a medium to long term timescale, taking into account the minimum period of time designated by the risk rating of the particular fund or portfolio, although this does not provide any guarantee that your objectives will be met. Please note that the content is based on the author’s opinion and is not intended as investment advice. It remains the responsibility of the financial adviser to verify the accuracy of the information and assess whether the OEIC fund or discretionary fund management model portfolio is suitable and appropriate for their customer.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 109.5.24