The Backdrop

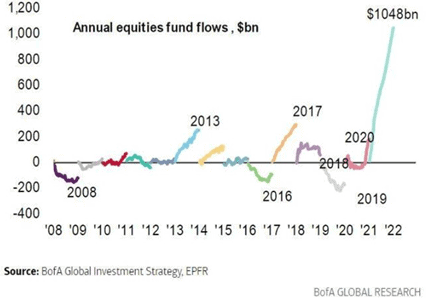

This article primarily focuses on the US markets because US equities now make up a staggering 69% of the main global indices. In addition, US markets have benefitted most from the low-interest rate environment. The US retail investor has dumped more of their savings into US stocks in 2021 than in any other year, in fact, more than the last few years combined. Overall, in 2021, approximately $1 trillion has been invested in the global equity markets, and that’s more than all other years of the last decade added together (fig 1). One final point to set the scene, although all countries have a central bank, no other central bank is as influential as the US Federal Reserve (Fed).

Annual Equity Fund Flows as of September 2021 | fig 1

Source: MarketWatch.com

Central Banks

There is an ongoing debate about whether the major central banks are now behind the curve of economic reality. Do they really believe the transitory inflation narrative for which evidence is diminishing literally by the day? Or are they trying to keep markets elevated by endless jawboning, whilst clinging to the hope that economically something terrible happens to justify their current monetary stance?

To be sure, the risks are considerable whatever course they take from here, as equity markets in the US have broken virtually every record so far in 2021. One crucial point that should not be overlooked is that the Fed controls markets by what it says, as much as what it does. So, just as with the diminishing effects of additional quantitative easing, how much more credible mileage is there in verbalising the transitory inflation supposition instead of acknowledging the actual inflation data, which essentially contradicts Powell’s comments? On 30th November 2021, Powell buckled under the reality of the data. He now thinks the word transitory should be retired, and in any case, “it meant different things to different people”. On this point, at least he is correct; even the existence of a planet is transitory.

What we do know is that the global low-interest rate club is rapidly disbanding. Some small central banks have already started raising rates -the period of lower for longer is over, as shown by central banks such as those in the Czech Republic and New Zealand. The Bank of England did signal that it was likely to raise rates in November, or at least that’s how most commentators saw it. In the end, they performed an ‘unreliable boyfriend’ performance that would have had Mark Carney blushing. Apparently, they wanted more definitive information on inflation and jobs.

Since the November meeting, there has been blow out data on both fronts, so surely a December rate rise is a certainty, you might think? Well, not so fast; Andrew Bailey is already giving himself and the rest of the team some wiggle room based on potentially deteriorating covid data. They might never get a better chance to re-set market expectations with a mere 25pbs raise. No move in December and the shouts of getting seriously behind the curve will potentially become deafening, but risk assets could once again potentially gain on central bank inertia.

To summarise, the same actions could beget precisely the same results.

Governments

At the same time, the major central banks are arguably adopting a strategy predicated on hope; we have the US government handing out cheques and passing substantial spending bills. This time it’s the Democrats, but Trump also juiced the stock markets during his (first?) tenure with his tax-cutting. Much of this free money also found its way into risk assets. So, the Democrats, the Republicans and the Fed agree on at least one thing; high equity markets make most voters and politicians very happy, and that it seems in their view cannot be a bad thing. Much of this fiscal largess has yet to even get into the system, let alone work through it, and it will add to inflationary pressures.

At this point, there is the first potential fly in the proverbial ointment. We can expect governments worldwide to have increasingly tense relations with their hitherto not very independent central banks. Higher equity markets will never, of course, be an explicit goal. Still, they are certainly an outcome of the actions of the US authorities, in particular. However, if central banks are needed to raise rates to curb the not so transitory inflation, where does that leave risk assets?

Winners and Losers

The stock market itself has been a clear winner from the fiscal and monetary policy, but there has been a third factor: the behaviour of investors themselves. Some sectors and indeed specific stocks have been on an incredible run. This now leaves them with some mind-boggling statistics and ratios to grow into, which are based on scenarios that at best seem highly improbable and are, in some cases, frankly absurd.

Buying any dip in the markets has been a very successful strategy in recent years, as has, chasing momentum plays in many cases. Some companies have seen their share prices go ‘to the moon’ whilst their fundamentals have frankly been going to the dogs. What will all the retail money do if the central banks can no longer unconditionally have the back of every long investor?

The New Winners

A new group of winners seemed extremely unlikely at the onset of the pandemic, but that is clearly employees. Vacancy rates have been at their highest levels for decades in many industries, and employers have been throwing money at new employees just to get them on to the books. Wages themselves continue to rise at a faster clip than has been seen for many years. Wages don’t tend to go backwards, and employers are struggling to keep up. In fact, it seems it’s only certain economists who don’t seem to be struggling to grasp what is happening in the real economy. All the evidence from people who actually employ people is that it’s a challenging environment right now, and they don’t see any signs of it getting easier any time soon.

Do fundamentals matter anymore?

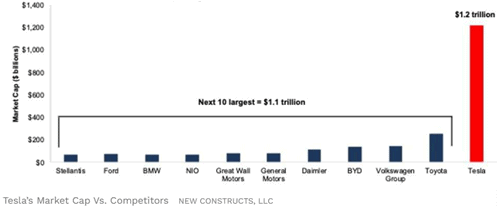

The P/E of Tesla is now just shy of 360, and it is valued at more than all of the world’s largest car companies, combined with a market cap of over $1 Trillion (fig 2 | as of November 9th). Whether Tesla is a great company or not is not the issue here, and neither is our views on the cult of Elon Musk. The infinitely more prescient point is that the price paid by an investor today might turn out to be of great significance if we do indeed start witnessing the end of super-easy monetary policy. Of course, the credibility of the valuations is not related to Tesla alone, but it is the poster child for the excesses or new paradigm in the current era, depending on your view.

Tesla Market Cap vs Competitors | fig 2

Source: Forbes

Inflation

There are numerous tailwinds behind the rapid increase in inflation. For a start, US wage growth is at approximately 5%, and savers have circa $2 trillion held in cash accounts. Added to that, many people don’t even want to come back into the labour market. They have made so much free money they have retired earlier and for good!

It has to be a possibility that we have an inflationary explosion caused by record amounts of fiscal stimulus colliding with super-loose monetary policy and hitting substantial pent-up demand. Whilst retiring the word transitory is at least an acknowledgement of economic reality, it will need to be followed up with actions. Most importantly for investors, what will the Fed response be if equity markets fall in response to their actions?

As the chip shortage gets resolved, certain areas like falling new car prices might get the headlines in 2022, but this is a relatively small component of recognised inflation. At the moment, at least we have re-escalated used car prices that supply pressures have hit, and this is data that is essentially yet to be reflected in CPI figures.

All these potential scenarios lead us to a rather unsatisfactory conclusion. Many people are guessing on inflation rates, but in reality, nobody knows for sure because this situation is genuinely unprecedented. The inflationary impact and subsequent interest rate move impact is also unknowable because the US has never had this much debt before either.

Labour trends have shifted markedly since the outbreak of covid, and the bottom 10% of earners have seen some of the most significant gains. These same strata of society are also more likely to spend any additional money, whether earned or a government cheque.

The often and correctly used inflation counterargument is that technology and demographics are generally deflationary. This is true, but inflation is here and now, not a few years down the road anymore. Until covid, you could have said the global economy had time on its side to improve efficiencies etc., before inflation might really bite, but that ship has since sailed.

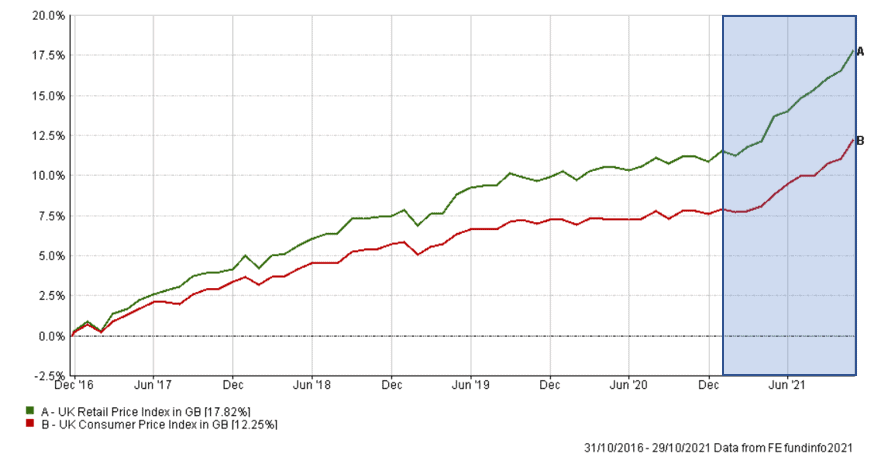

CPI & RPI Over 5 Years to 29/10/2021 | fig 3

The Outlook for Risk Assets

If the Fed doesn’t act somewhat more aggressively than is currently priced into markets and inflation keeps spiralling upwards, at some point their hands will be forced, which could be very bad for risk assets. As record amounts of retail money have flowed into US equities, a sell-off in tech caused by interest rate rises could be more significant than at any time since the end of the dot.com bubble.

Suppose, then, they do act sooner rather than later. In that case, this could also be bad for those very same assets which have prospered over the last decade as so many investors are treating the current market conditions as though they will persist indefinitely.

A third scenario is that economic growth gently rolls over and inflation subsides, and the Fed never really act. In that case, the party can continue, but that will obviously hit earnings and ultimately cannot be good for risk assets other than ones potentially that thrive on lower forever rates. So, maybe Tesla goes to 500 times forward earnings! You would probably also see more government stimulus that would either restart the inflation engine, or one of the above scenarios is merely delayed. Alternatively, if the stimulus fails to energise the economy sufficiently, the pressures on earnings would prevail, and yet possibly, the effect could still be inflationary.

If risk assets tank, the Fed may well try to step back in either through jawboning or reversing any tightening measure so far deployed (if any). However, this could be the moment when markets cannot be convinced that the Fed has its back, and then we hit a significant air pocket taking equities back down to something approaching a stock’s fundamentals. At this point, the investment thesis of acronyms TINA, FOMO and BTD etc., could face their most severe test yet.

Markets have never been more convinced than they are now that central banks have them covered. We absolutely agree with that supposition. The question, however, remains, what happens when an event or phenomenon such as rising inflation happens and the leading central banks cannot or won’t act to prop up markets?

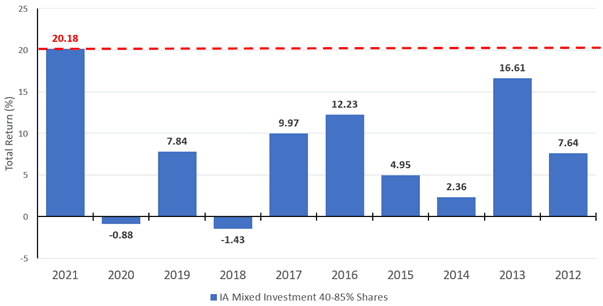

We have not reached the point of retesting central bank resilience, and it may be many months or even years, which is why markets can continue to climb awhile yet from here. The reason multi-asset sectors such as the IA ones are having their best rolling year ever (fig 4) is because we have reached either maximum optimism or maximum greed. It seems to us that when you have valuations such as that of Tesla, FAANMGs making up over 25% of the S&P and rapidly rising inflation, we should be proceeding with caution.

Something will deflate the everything bubble, and we have to hope that the central banks led by the Fed play the game of their lives. Hope, however, is not an investment strategy, and the data says it’s going to be a tough fight for them.

IA Mixed Investment 40-85% Shares Rolling 1 Year Returns to 31/10/2021 | fig 4

Conclusion

We think inflation is here to stay, so that leaves us with two questions.

Firstly, how do the central banks deal with it?

Secondly, and perhaps as crucially, what happens to all that money that has so recently been invested if buying the dip turns out to be more akin to catching a falling knife?

So, regardless of the outcome from here, we feel it is prudent to have minimal exposure to assets that are at, or near, their all-time highs, that have benefitted from extraordinary monetary policy and ensure we have high levels of diversification within all our investments.

This communication is designed for professional financial advisers only and is not approved for direct marketing with individual clients. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Please note that the content is based on the author’s opinion at the time of writing/publish date. Our views and opinions regarding certain investment themes and topics can alter over time as the macroeconomic background changes and other industry news is made publicly available, this is not intended as investment advice.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

Data is provided by Financial Express (FE). Care has been taken to ensure that the information is correct but FE neither warrants, neither represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Please note FE data should only be given to retail clients if the IFA firm has the relevant licence with FE.

IBOSS Asset Management is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Limited (Portfolio Management Service) is a non-regulated organisation and provides model portfolio research and outsourced white labelling administration service to support IFA firms, it is owned by the same Group, METNOR Group Holding Limited who own IBOSS Asset Management Limited.

Registered Office is the same: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 381.12.21