While attention often gravitates towards the S&P 500 and Nasdaq 100 indices making new highs, the UK has quietly claimed the top spot among developed equity markets in Q2 2024, so far, in sterling terms (Fig. 1).

Performance Line Chart – 01/04/2024 to 20/06/2024 (Fig. 1)

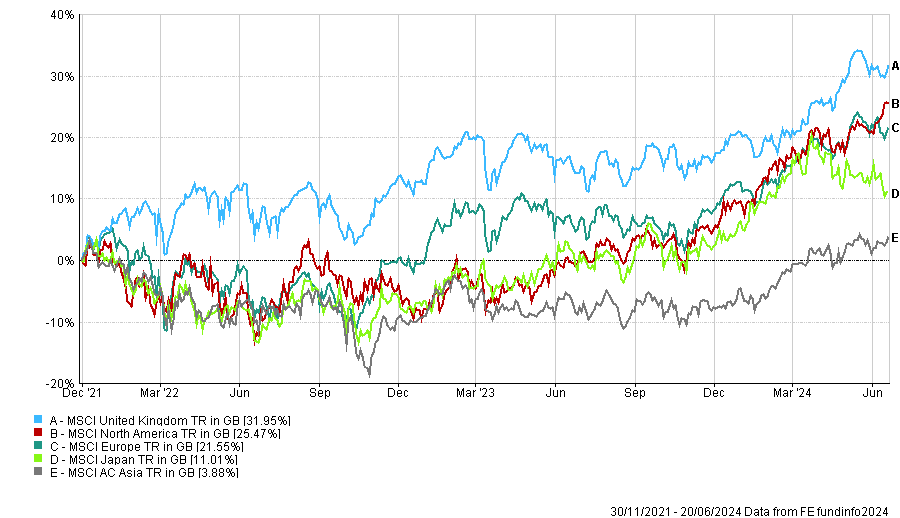

The UK Stock market has suffered from a poor public image over recent years. However, amid the ongoing discourse around American exceptionalism, since November 30, 2021 – around the time Federal Reserve Chair, Jerome Powell, acknowledged the Fed’s missteps regarding ‘transitory’ inflation and embarked on the fastest rate hike cycle in modern history – the UK market, as measured by the MSCI, has outperformed North America by 6.5% in sterling terms, as of June 20, 2024 (Fig. 2).

Performance Line Chart – 30/11/2021 to 20/06/2024 (Fig. 2)

Factors Driving the Recent Turn in Sentiment

Several factors have contributed to the recent resurgence of the UK equity market. Inflationary impacts abating, real wage growth, coupled with hopes of lower interest rates and economic stability, have played significant roles as improvements to GDP, consumer confidence, and manufacturing PMI have seen off a mild recession. Furthermore, optimism surrounding the Bank of England’s interest rate decisions and the global economic outlook have also positively impacted investor sentiment, leading to increased market activity.

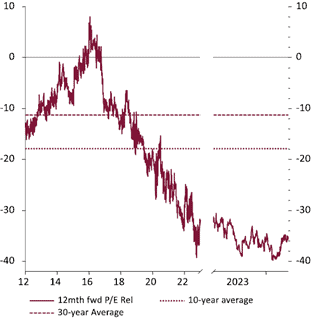

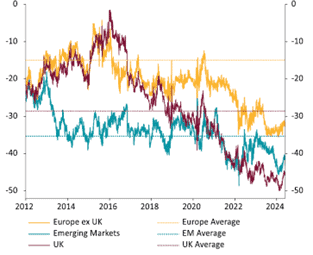

Recent data indicates that the UK equity market trades at a discount relative to history and global counterparts. Specifically, it trades at a 35% markdown relative to the rest of the world (Fig. 3) and a significant 45% discount compared to US equities (Fig.4).

This attractive valuation is complemented by robust buybacks and dividend yields, that are nearing decade highs.

UK % P/E Discount Relative to Rest of World (Fig.3)

Source: Kingswood Group

% P/E Discount Relative to US Equities (Fig.4)

Source: Kingswood Group

2023 saw 39 UK companies with market capitalisations exceeding £100 million become bid targets, commanding an average premium of 58%. So far in 2024, the FTSE 250 has experienced a surge in merger and acquisition activity, with notable bids on 4% of constituent companies alone.

Untapped Potential & a Calmer Backdrop in the UK

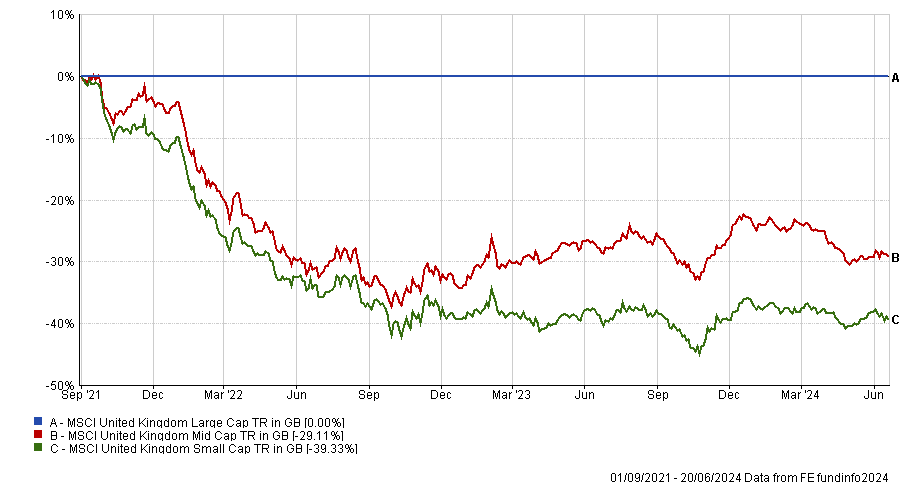

Despite recent gains, the FTSE 100 still trades below its long-term average, signalling potential room for further growth. Equally compelling is the valuation disparity between large-cap and mid/small-cap companies within the UK market. Since September 2021, the MSCI UK Mid Cap and Small Cap indices have underperformed their large-cap counterpart by approximately 29% and 39%, respectively (Fig. 5).

This valuation gap, coupled with a more stable political environment and improving domestic economic fundamentals, presents promising opportunities for UK SMID (small and medium-sized enterprises) sectors.

Performance Line Chart – 01/09/2021 to 20/06/2024 (Fig. 5)

The global geo-political backdrop is decidedly mixed. Firstly, there are the ongoing conflicts in the Middle East and Ukraine. Then there are wars of words, tariffs, and counter-tariffs, notably between the US and China, but also between many other countries. Alongside these issues, a record number of countries voters are going to the polls this year. As the UK general election is the next one on the horizon, polling suggests the next government could have one of the strongest mandates in modern history, with both the US & Europe’s political backdrops appearing potentially more turbulent than the UK’s. The offer of stability and a predictable but credible post-election policy plan could be another positive catalyst for Pound Sterling and UK assets.

Research suggests historical performance isn’t a good indicator in predicting the performance of UK equities under future governments. Since June 1970, under Conservative governments the FTSE 350 has generated a higher real total return in sterling terms. While in dollar terms, the FTSE 350 has generated better relative performance against MSCI World under Labour governments. This suggests, the primary influences are unlikely to be associated to the political party, but rather the prevailing economic conditions.

IBOSS’s Position

As multi-asset investors, we leave the underlying stock picks to the fund managers in whom we place our trust. Speaking with our UK managers some have positioned accordingly in response to potential leadership changes by avoiding sectors they view as could be directly impacted by a change to a Labour government, such as rail companies (due to the risk of nationalisation) and major oil (due to the continuation of windfall taxes). Conversely, the easing of planning regulations and greater commitment to social housing is seen as a potential long-term opportunity for the housing sector.

Both Labour and Conservative parties have committed to not raising national insurance, income tax or VAT. Neither party can risk radical policy initiatives, and whoever enters government will be tied by tough fiscal rules.

Our current UK equity allocation in our most popular portfolio, Core portfolio 4, is 16.15%. We hold multiple managers in the sector and blend various investment styles. Our portfolios are exposed across the market cap scale encompassing large, medium and small sized companies. With the economic and political backdrops improving, we remain optimistic on the UK and the upcoming election could further enhance the perception of the UK among domestic and international investors.

This communication is designed for informational purposes only and is not intended as investment advice. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Please note that the content is based on the author’s opinion at the time of writing/publish date. Our views and opinions regarding certain investment themes and topics can alter over time as the macroeconomic background changes and other industry news is made publicly available, this is not intended as investment advice.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 136.6.24