Setting the Table

As everyone, and their bank accounts, is undoubtedly aware, inflation is now well and truly in the system. Headline inflation has dropped from 8.9% in March 2023 to 3.8%, which, whilst clearly good news, still indicates a significant rise in the price of goods and services over the past few years.

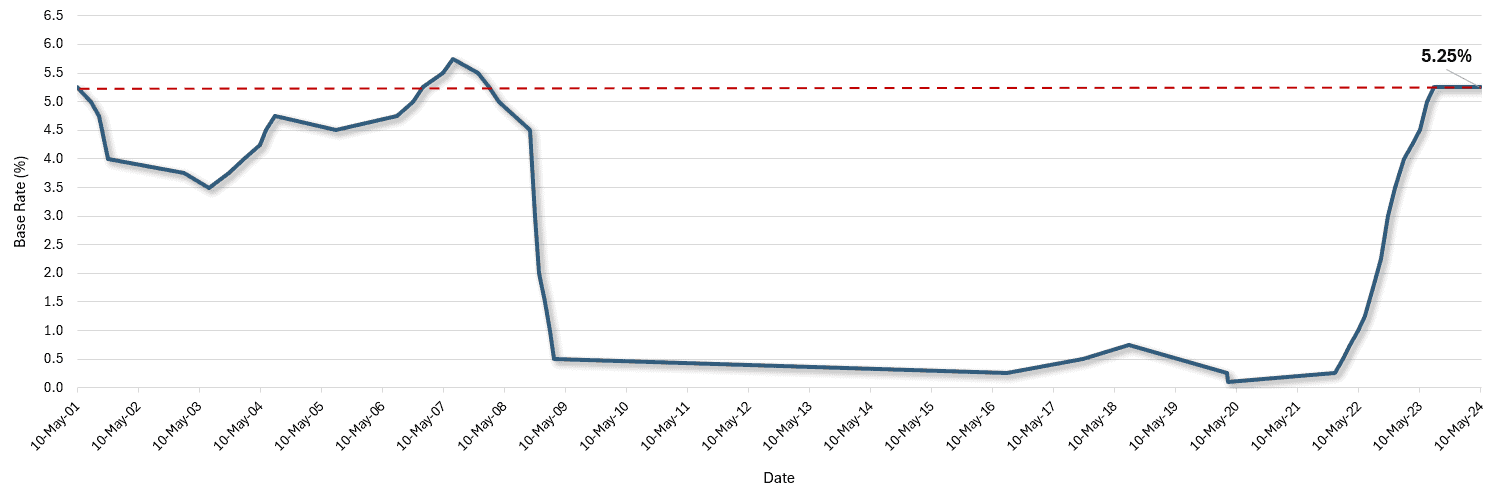

As a necessary response, central banks have increased interest rates. The Bank of England base rate has rose from 0.1% at the end of 2021 to 5.25%, a rate we haven’t seen since February 2008. In fact, interest rates have been under 1% since February 2009. In short, the investment world had, until recently, been used to low rates for almost 15 years (fig 1).

Bank of England Bank Rate (10/05/2021 – 10/05/2024)(fig 1)

Source: Bank of England

Asset prices are keenly affected by changes in interest rates and many have experienced lacklustre returns in the face of rising rates.

However, now that the dust has almost settled and rates are at least closer to peaking, it is time to re-assess the menu of assets available to investors and try to identify those that can outperform from here, rather than focus on a low-interest environment that no longer exists.

The Death of the 60/40 Portfolio

In a low-rate, low-inflation environment, attractively yielding and non-correlated assets were incredibly hard to come by.

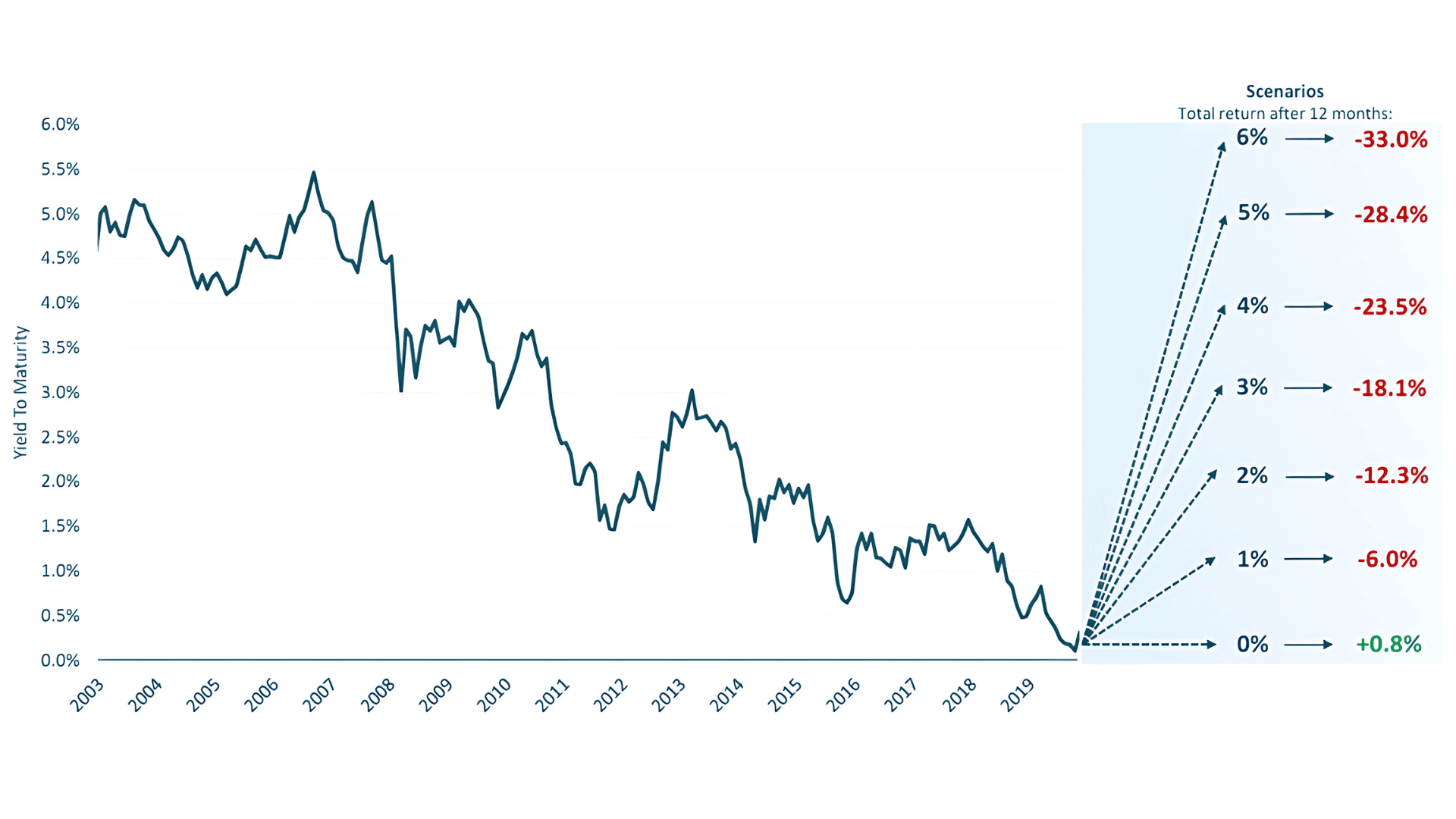

Traditionally, fixed income assets fulfilled this brief, but the chart below (fig 2) highlights the 10-year Gilt risk vs return scenario at the end of 2020. In short, you got almost no yield and any movement higher in interest rates would severely impact your capital. Ultimately, this proved the case and the average bond fund fell circa 23% in 2022 and 33% peak to trough.

10-year Gilt Scenario as of 2020 (fig 2)

Source: M&G

With traditional bonds out of the picture, investors were forced to look elsewhere for these non-correlated and yielding characteristics. As such, we saw more complex vehicles surfaces to fill the gaps in the form of structured products, absolute return funds, and even more obscure solutions like aircraft hangers and residential property funds.

I’ll Take a Margherita Pizza and Vanilla Ice Cream Please!

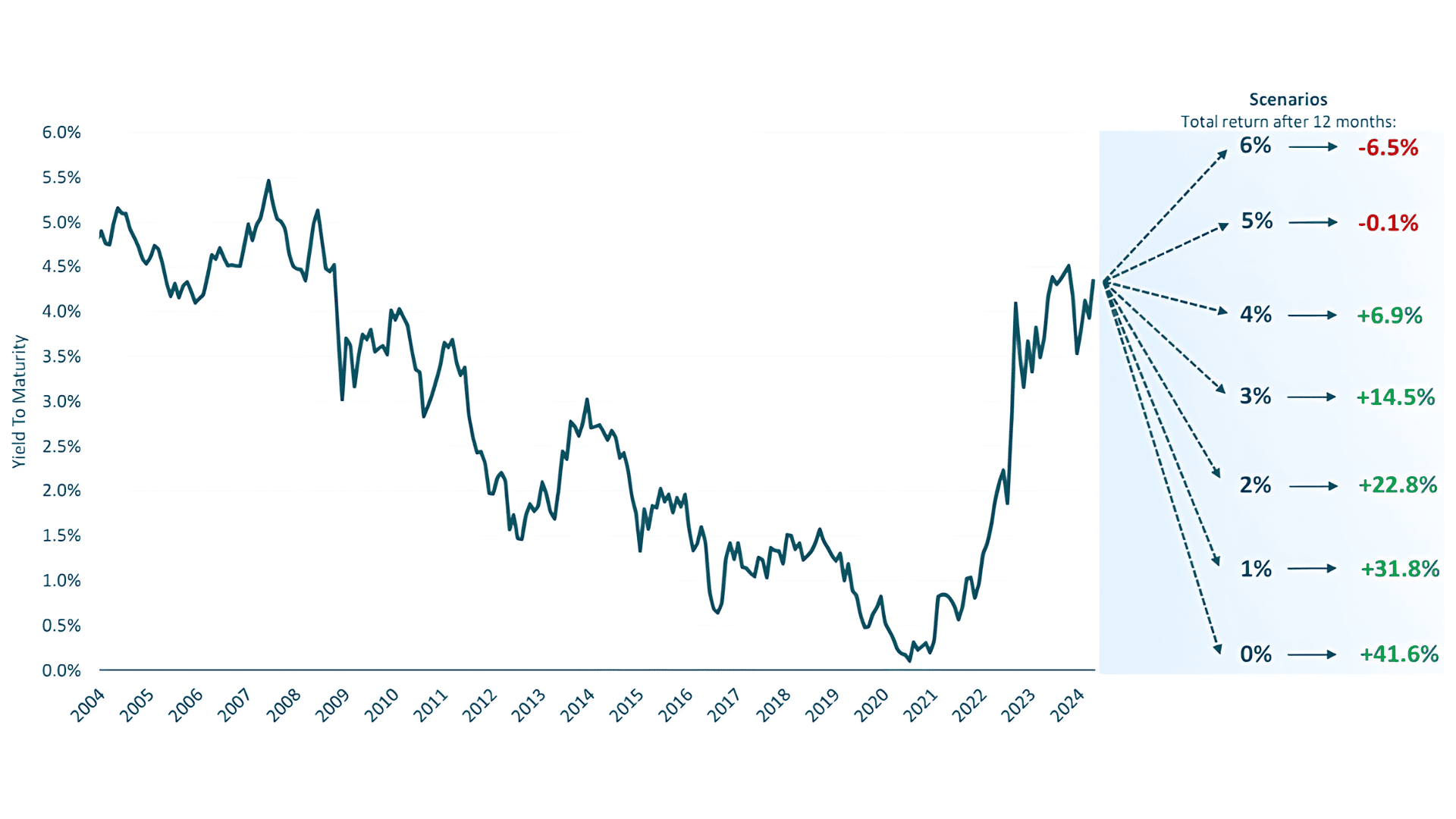

Things have now changed. The chart below (fig 3) shows the same scenario analysis but as of this year and following the various interest rate hikes. As you can see, not only do bonds offer a much more attractive yield, but there is also the potential for real capital growth if yields fall.

Ultimately, we can’t say where interest rates go from here, but the risk/return profile is much more positively skewed than it has been over recent history.

As such, we have been increasing the duration of our bonds, broadening the portfolio’s exposure to a variety of different bonds, and increasing the allocation to active managers over passive. This last point highlights our view: that with rates higher, active managers have more tools to play with than in recent years and should therefore be well-positioned to benefit.

10-year Gilt Scenario as of 2024 (fig 3)

Source: M&G

This takes us to the crux of this month’s blog, and the tenuous link to foodstuffs. In a low-interest rate environment, the case could have been made to invest in complicated solutions to adapt to a limited opportunity set.

But much like the classic margherita pizza or vanilla ice cream, bonds are seen as a fairly mundane investment choice, but they are classics for a reason, and as interest rates have risen so too has the opportunity set. We contend that whilst some more complicated investment solutions may work from here, many are tackling a yield problem that no longer exists and we believe that there is a significant benefit to be had by keeping it simple.

This communication is designed for informational purposes only and is not intended as investment advice. These investments are not suitable for everyone, and you should obtain expert advice from a professional financial adviser. Please note that the content is based on the author’s opinion at the time of writing/publish date. Our views and opinions regarding certain investment themes and topics can alter over time as the macroeconomic background changes and other industry news is made publicly available, this is not intended as investment advice.

Past performance is not a reliable indicator of future performance. The value of investments and the income derived from them can fall as well as rise, and investors may get back less than they invested.

IBOSS Asset Management Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register Number 697866.

IBOSS Asset Management Limited is owned by Kingswood Holdings Limited, an AIM Listed company incorporated in Guernsey (registered number: 42316).

Registered Office: 2 Sceptre House, Hornbeam Square North, Harrogate, HG2 8PB. Registered in England No: 6427223.

IAM 115.5.24